SDE vs. EBITDA: Why the Distinction Changes Your Deal

Jul 05, 2026

Two owners, both running profitable businesses, both asking the same question: what is my business worth?

The answer for one of them is calculated on SDE. The answer for the other is calculated on EBITDA. The distinction between the two is not just a technical accounting difference. It changes the buyer pool, the financing options, the multiple range, and the way the deal gets structured. Getting this wrong can mean going to market with the wrong number, attracting the wrong buyers, and leaving money on the table.

What SDE is and when it applies

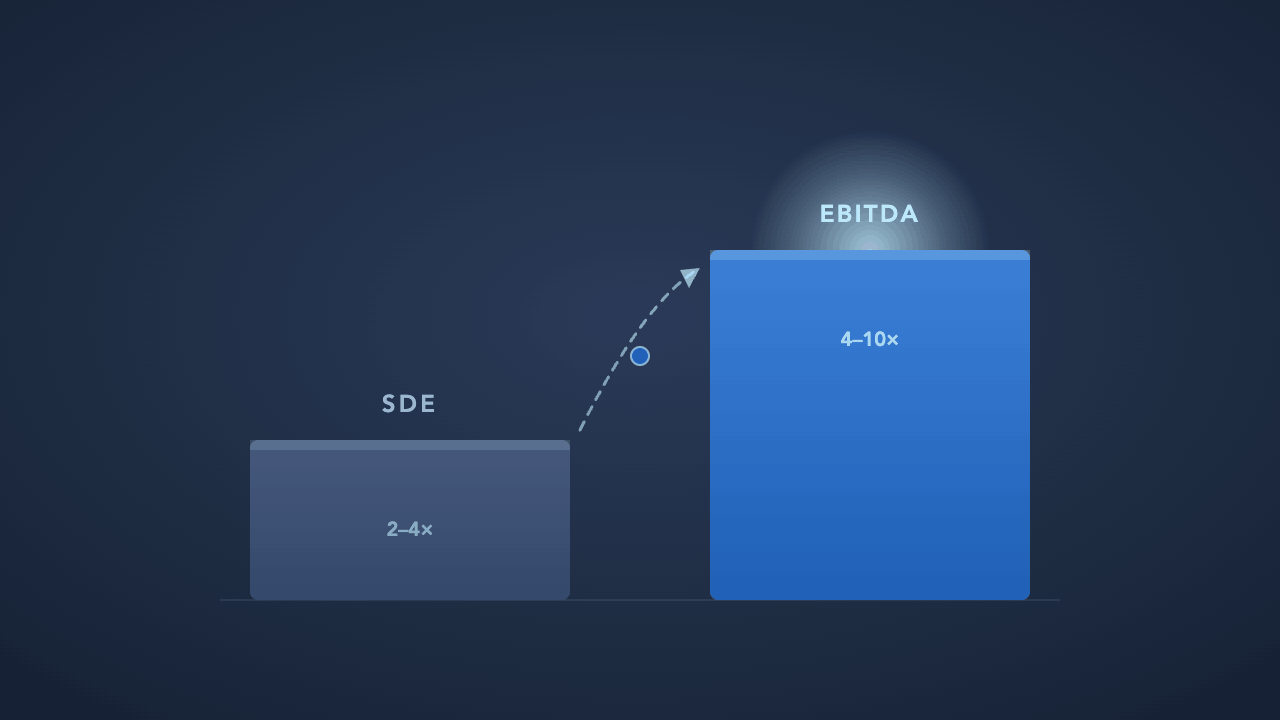

SDE stands for Seller’s Discretionary Earnings. It starts with net income and adds back the owner’s full compensation and benefits, taxes, depreciation and amortization, interest, and any other personal or one-time expenses run through the business. The logic is that SDE represents the total economic benefit available to a single owner-operator who steps in and runs the business themselves.

SDE is the right metric for smaller businesses, generally those with revenue below $2M to $3M, where the buyer is expected to be an owner-operator working in the business full time. The buyer gets to replace the existing owner’s salary with their own, so the full owner benefit is relevant to pricing.

Typical SDE multiples in this range run from 2x to 4x, depending on industry, growth, and risk profile. The buyer pool is primarily individual operators, search fund buyers, and small holding companies.

What EBITDA is and when it applies

EBITDA stands for Earnings Before Interest, Taxes, Depreciation, and Amortization. Unlike SDE, it does not add back the full owner compensation. Instead, it assumes a market-rate salary for a professional manager is already in the expense base, or adjusts to include one. EBITDA measures the operating cash generation of the business independent of the owner’s personal compensation structure.

EBITDA is the right metric for businesses that have or can support a professional management layer, generally those with revenue above $3M to $5M. The buyer is not expected to operate the business themselves. They are buying the earnings stream.

EBITDA multiples in this range start around 3x to 4x at the low end and can run to 8x, 10x, or higher for businesses with strong recurring revenue, low customer concentration, and a proven management team. The buyer pool expands significantly: private equity, family offices, strategic acquirers, and search funds all participate.

Why the crossover matters

The transition from SDE pricing to EBITDA pricing is one of the most important inflection points in a business’s value trajectory. A business generating $500K in SDE and priced at 3x is worth $1.5M. A business generating $1.5M in EBITDA and priced at 5x is worth $7.5M. The underlying business might not be that different in size. The pricing framework is entirely different.

The crossover is not automatic. A business at $4M in revenue that still depends entirely on the owner, has no management layer, and has no documented systems is still an SDE business regardless of its revenue. It attracts owner-operator buyers and prices accordingly.

A business at $3M in revenue with a real GM, recurring revenue, and clean financials may already be crossing into EBITDA territory, attracting a more sophisticated buyer pool and commanding a higher multiple.

The threshold is not revenue. It is infrastructure.

What this means for how you prepare

If you are pricing on SDE and your business is approaching the crossover point, it is worth asking whether you can get to EBITDA pricing before you go to market. The answer is usually yes, but it takes time. Hiring the GM, cleaning up the financials, and demonstrating that the business runs without you are the prerequisites. None of those happen in a quarter.

If you are already in EBITDA territory, the question shifts to multiple expansion. What would move your multiple from 4x to 6x? Usually it is revenue quality, customer concentration, growth rate, and the strength of the management team. Those are also multi-year projects.

When clients hire me, this is one of the early conversations. Which metric are you being priced on, and what would it take to move up the stack? The answers shape the entire preparation timeline. Know which number you are, and know what it would take to become the other one.

Want to work one-on-one with me to get your business exit-ready? Apply now to schedule a free call where we go over your business in detail. Apply for a FREE Call Now >>

If you didn’t know, now you know.

* Every deal I look at is under NDA. The stories I discuss are real. Some identifying details — company name, specific geography, exact numbers — may have been changed to protect the seller. The lessons haven’t.