Why EBITDA Is a Starting Point, Not a Price

Jul 04, 2026

I talk to owners every week who know their EBITDA and have a multiple in mind. They have done the math. If the business does $1.5M in EBITDA and the market trades at 5x, they should get $7.5M.

Sometimes that is right. Often it is not. And the gap between the number the owner expects and the number the buyer writes is almost never a disagreement about the multiple. It is a disagreement about the EBITDA.

The buyer’s EBITDA is not your EBITDA

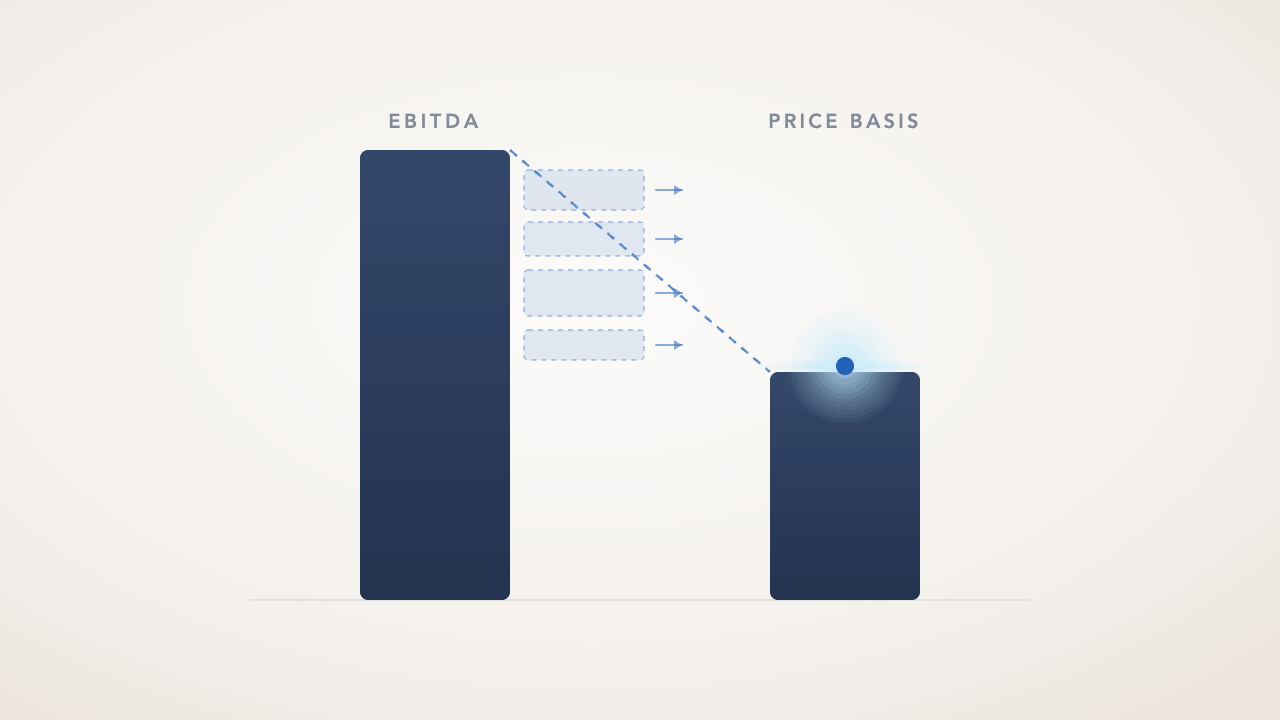

Your EBITDA is the number on your financial statements after your accountant has made your taxes as efficient as possible. The buyer’s EBITDA is the number after a quality of earnings team has gone through every line and asked whether it belongs there.

Those two numbers are almost never the same.

The QofE process, short for quality of earnings, is a forensic examination of your financials. The buyer’s accountants are looking for revenue that is not recurring, expenses that are understated, add-backs that do not survive scrutiny, and working capital dynamics that affect what the business actually produces in cash. Every adjustment they make goes directly to the EBITDA number the multiple gets applied to.

A $1.5M EBITDA with $300K of adjustments going the wrong way is a $1.2M EBITDA. At 5x, that is a $1.5M difference in purchase price. That is not a rounding error.

The adjustments that move the number most

Not all adjustments are equal. These are the ones I see change valuations most significantly.

- Undefended add-backs. Owners add back personal expenses, one-time costs, and owner compensation with varying degrees of documentation. Every add-back the buyer’s team cannot verify with receipts, payroll records, or clear categorization gets rejected. The add-back schedule is where deals quietly lose value.

- Revenue normalization. A contract that ended. A one-time project that inflated last year’s top line. A customer who has already signaled they are reducing volume. Buyers will strip out revenue they cannot underwrite as recurring, and that goes straight to EBITDA.

- Run-rate vs. trailing twelve months. If revenue is declining, buyers want to price on a run-rate that reflects the current trajectory, not the trailing twelve months that include a stronger period. If revenue is growing, the seller wants credit for the trend. This negotiation happens at the EBITDA level, not the multiple level.

- Owner compensation replacement cost. If the owner is paid below market, the buyer will add the cost of replacing them at market rate to the expense base. If the owner is paid above market, some of that comes back as an add-back. Either way, the number shifts.

- Capex requirements. EBITDA does not include capital expenditures. A business that requires $300K of annual capex to maintain its equipment and systems is not producing the same free cash flow as a business that requires $30K. Buyers price this into their effective multiple even when the headline multiple looks the same.

What this means for how you prepare

The owners who get the best outcomes are the ones who understand their own EBITDA the way a buyer will see it before anyone else does. They have run the add-back schedule with documentation behind every line. They know which revenue items a buyer will challenge. They have done their own working capital analysis so there are no surprises at the closing table.

When clients hire me, this is often where the most important work happens. Not on the strategy, not on the banker selection, but on understanding the gap between the number the owner believes they have and the number a buyer will actually pay on. Closing that gap before the process starts is the difference between a smooth diligence process and a painful retrade conversation.

EBITDA is where you start. What the buyer pays is determined by everything that happens between the first conversation and the closing table. Know your number. Know how it will look under a microscope. And close the gaps before someone else finds them.

Want to work one-on-one with me to get your business exit-ready? Apply now to schedule a free call where we go over your business in detail. Apply for a FREE Call Now >>

If you didn’t know, now you know.

* Every deal I look at is under NDA. The stories I discuss are real. Some identifying details — company name, specific geography, exact numbers — may have been changed to protect the seller. The lessons haven’t.